Wat Tyler posted an entry on his excellent Burning Our Money blog, pointing out that yesterday's interest-rate hike was a positive sign that the Bank of England Monetary Policy Committee were deciding to get back on top of inflation, not a disaster for an economy, as it was reported by much of the mainstream press. As usual, Wat is quite right, but I questioned the final part of his post:

"this time through all those pensioners, widows and orphans who've invested their savings in fixed income debt such as government bonds will be protected. For the first time since we abandoned the Gold Standard....Let us all give thanks for sound money."

I questioned not whether an increase in interest rates is necessary, but whether it is sufficient. Is it sufficient, for the purposes of maintaining sound money, to target changes in inflation indices with interest-rate adjustments, or can those inflation indices be misleading? In particular, I questioned whether expansion of the money supply and net sale/consumption of capital could conspire to give the appearance of only modest inflation (according to price indices) when the real value of our money and national wealth was falling faster than the indices indicated.

CityUnslicker replied rightly that I need to take account of the creation of capital in that calculation. I am posting a response to that point on this site, because I wanted to examine in more detail the inflow, outflow, creation and consumption of capital, and could not include graphics in the comments on the BOM site.

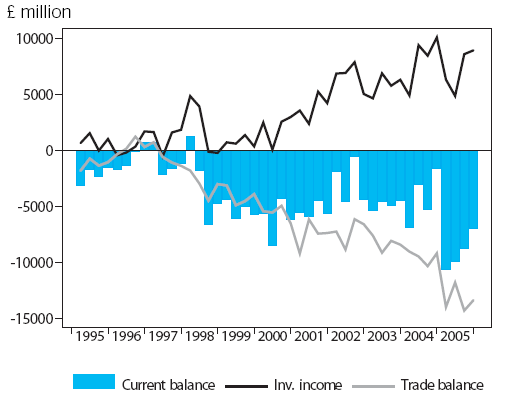

The latest edition of the Office for National Statistics' Economic Trends publication includes the following graph illustrating the trend in the Balance of Payments:

Clearly, the balance has been deteriorating for the life of this Government, even taking into account the positive contribution of inflows of foreign "investment" money. Relative to the size of our economy, our debts and our broad money supply, the outflows are not that big, but relative to the size of the narrow money supply, they are significant. So are we taking creating capital sufficiently fast relative to any consumption of capital, for it to compensate for net outflows of around £8 billion per quarter. That's quite a task.

Given the high rate of money-supply expansion, if we were succeeding in that task, would our nominal GDP growth not be higher? Would inflation not be higher? I'm really asking if there is another explanation - what else, apart from net consumption and export, could cause inflation to be significantly lower than than money-supply growth?

If there is not an alternative explanation, then our current behaviour is unsustainable. We are selling our futures and driving our nation towards bankruptcy (or, in practice, a harsh readjustment when reality finally bites).

| Attachment | Size |

|---|---|

| 34.69 KB |

{kind=link}